How student loan debt has increased over time

Canva

How student loan debt has increased over time

Students hold their diplomas at a college graduation

Some of the most common types of debt—a mortgage, an auto loan, and a credit card balance—are often necessary forms of debt people take on for everyday life, from covering household purchases and building good credit to attaining the American Dream of home ownership.

In the U.S., pursuing higher education has also often meant adding on another type of debt burden. Since The Great Recession, rising tuition at U.S. universities has contributed to student loans growing at rates unseen with other forms of personal debt. As of June 2022, the average student loan debt among consumers in the U.S. totaled $39,381, according to Experian. In 2012, U.S. consumers’ overall student loan debt surpassed the $1 trillion mark for the first time, and it’s continued its climb since.

To better understand how student loan debt has grown over time, Experian compiled data collected from student loan holders from across the country and government data dating back to 2009. The average loan balance used in the analysis represents the average debt among all student loan borrowers.

Historical data shows how average student loan debt balances have increased faster than inflation. In fact, student debt has also grown to equal more than credit card and auto loan balances combined.

![]()

Experian

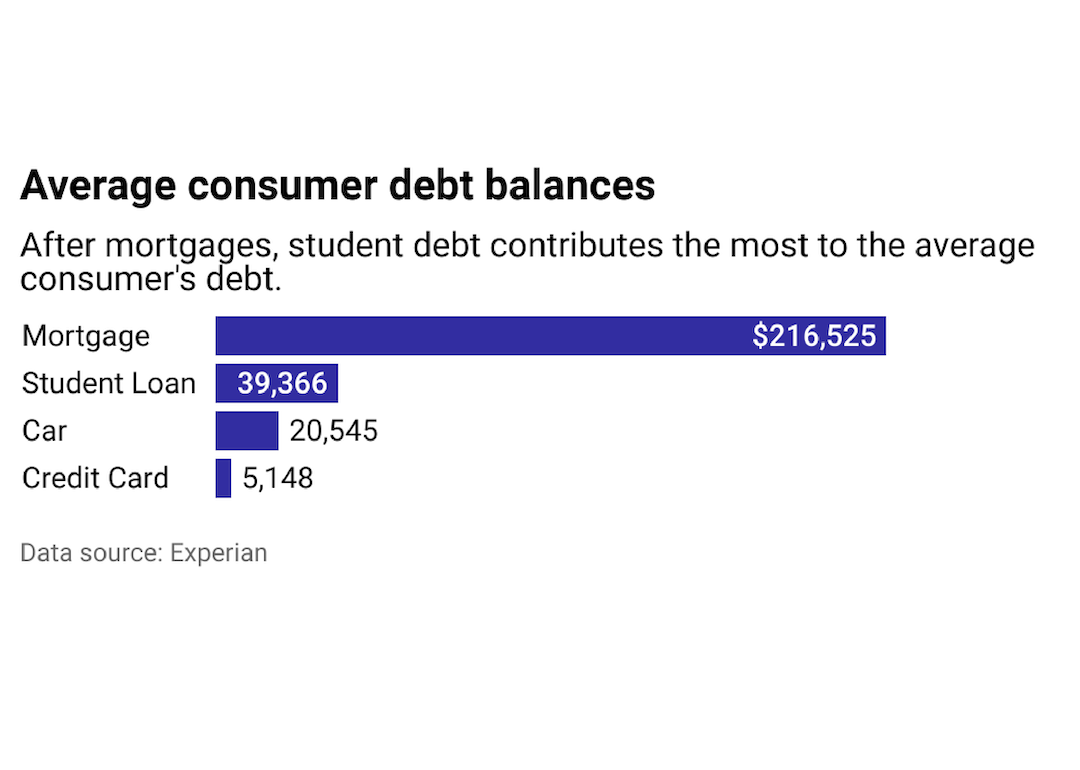

Student loan debt is the biggest form of debt after mortgages

Average debt balance by loan type.

As of Q2 2021, the average student loan debt balance has grown by nearly 92% since 2009, according to Experian data. Student loan debt averages saw the biggest year-over-year increase from summer 2012 to summer 2013 when they jumped nearly 10%. For Americans who carry student loan debt, it averages nearly $40,000—second only to home mortgages when it comes to consumers’ average debt balance.

Experian

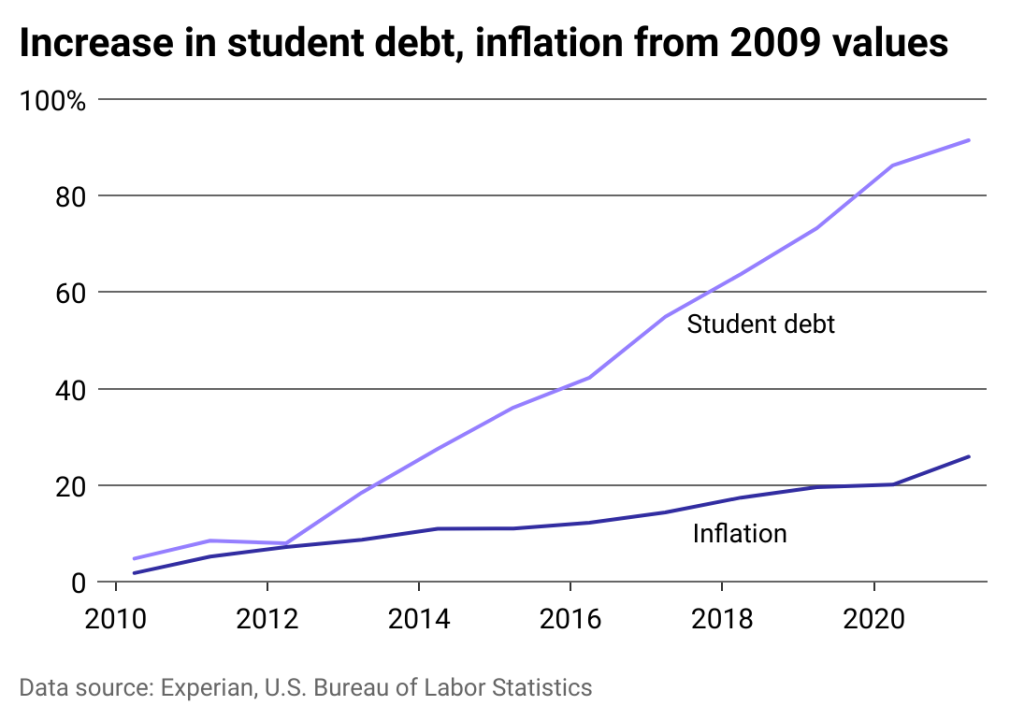

Student loan debt growth is outpacing inflation

Average student debt compared to inflation.

According to the U.S. Bureau of Labor Statistics (BLS), the annual nationwide inflation rate in the U.S. hovered around 2%—and often fell below 2%—over the decade leading up to the COVID-19 pandemic. In 2021, the first full pandemic-era calendar year, the inflation rate spiked to 7%.

Since the summer of 2012, the average student loan balance has grown much more rapidly. Over the three-year period preceding 2012, the average student loan balance grew by just under $2,000. Since 2012, student debt rose steadily at a much faster rate than income.

Experian

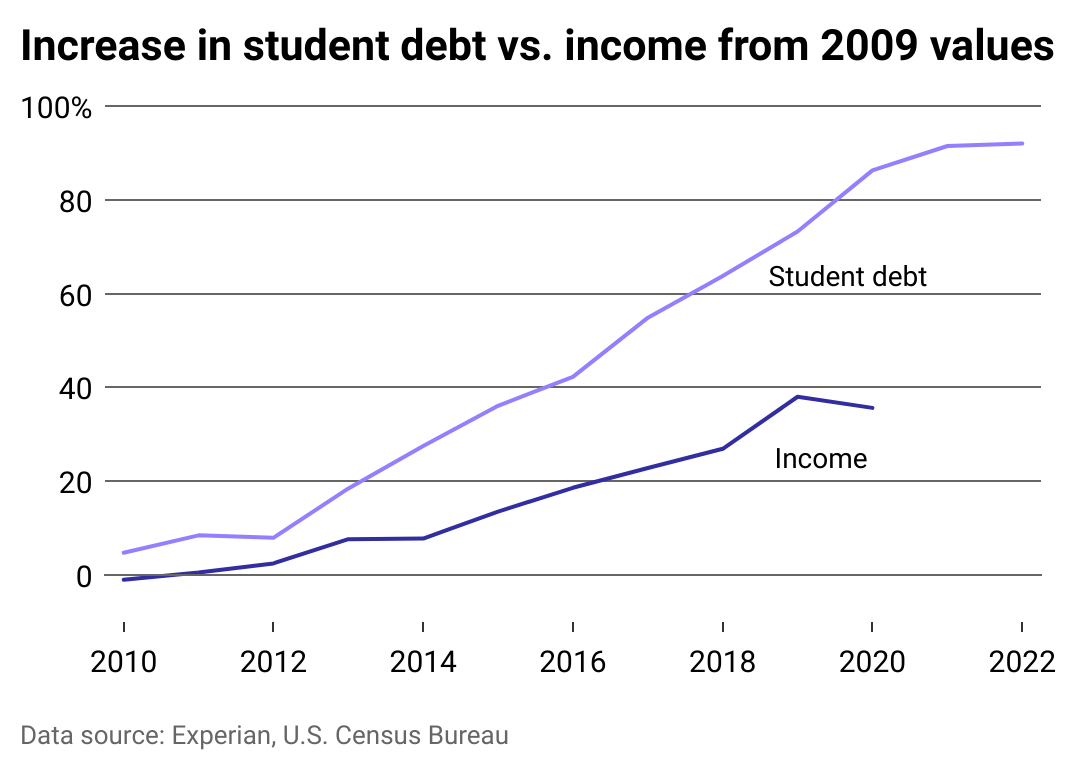

Student loan debt is outpacing income

Average student debt compared to the median household income.

The median household income in the U.S. fell in the years following the financial crisis of 2008, and then saw modest year-over-year growth from 2015 to 2020, according to the U.S. Census Bureau.

Comparatively, the average student loan debt balance has increased at more than twice the rate of the median household income since 2009. By 2020, the median household income had grown from $49,777 to $67,521, or about 36%, not adjusting for inflation. Between 2009 and June 2022, the average student loan balance held by U.S. consumers grew about 92%, from $20,560 to $39,381.

Experian

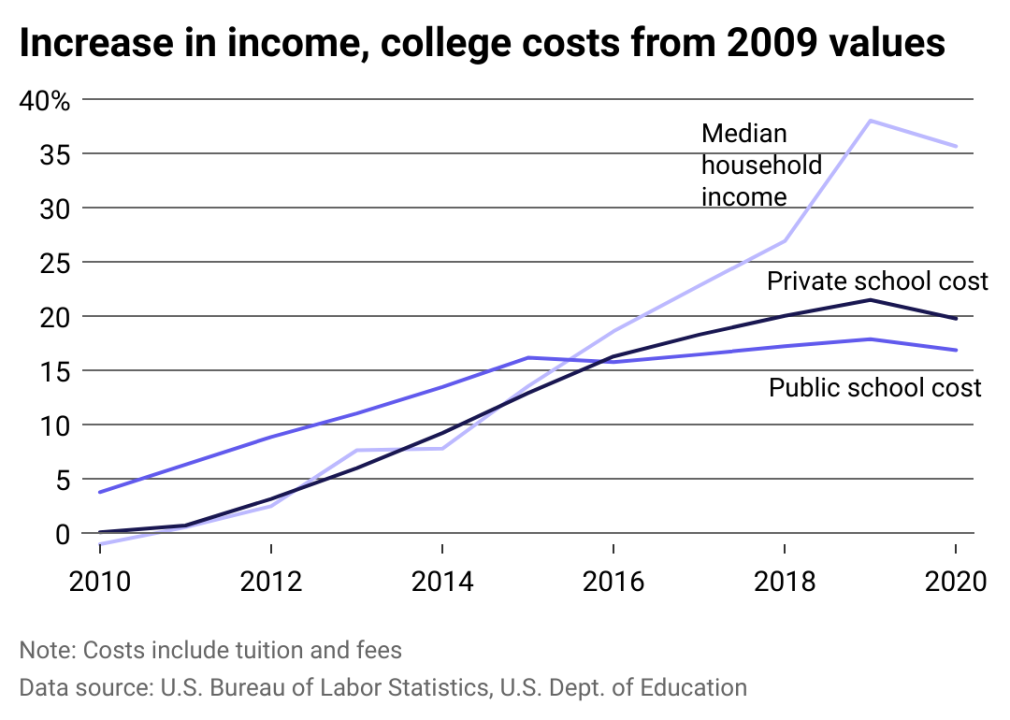

Growing college costs adding to financial strain

Average price of college compared to the median household income.

For at least a decade, college tuition has become increasingly expensive, according to data from BLS and the U.S. Department of Education.

The rate at which the average student loan debt balance in the U.S. has increased actually slowed from 2020 to 2021, according to Experian data. This is largely due to a nationwide drop in college enrollment during the COVID-19 pandemic, which reduced the number of people who took out new loans.

The CARES Act, passed in March 2020, also affected loan balances when it set an emergency relief interest rate for federal student loans at 0%. The law also allows employers to make up to $5,250 in tax-free annual payments toward their employees’ student loans, which could have had an effect.

On August 24, 2022, the Biden administration announced a student debt relief plan to cancel $10,000 in student debt for individuals making less than $125,000 a year, or $250,000 for married couples. Pell Grant recipients will receive $20,000 in loan forgiveness. For all borrowers, the pause on federal loan repayment has been extended for more than two years now, with a final deadline of December 31, 2022.

This story originally appeared on Experian and was produced and

distributed in partnership with Stacker Studio.